Tripura ranks as an ‘Achiever’ in NITI Aayog’s 2026 Fiscal Health Index. Explore how the state slashed its deficit to 0.8% and improved debt sustainability.

Agartala Mar 13: Tripura has officially entered the “Achiever” circle in the 2026 Fiscal Health Index (FHI), driven by a dramatic improvement in debt sustainability. According to the latest NITI Aayog assessments, the state’s debt-to-GSDP ratio plummeted from 32% to 27%, a shift that has redefined its economic standing among Northeastern and Himalayan states.

While the state still grapples with a heavy reliance on central grants, its ability to keep the fiscal deficit at a mere 0.8%—well below the national 3% ceiling—marks a significant milestone in State’s journey toward long-term fiscal consolidation.

Moreover, the government increased capital expenditure. It mainly directed this spending toward social and economic services linked to development priorities.

However, the fiscal structure still faces clear constraints. A large portion of the state’s revenue receipts continues to come from grants-in-aid and its share of Union taxes. In contrast, non-tax revenue remains very limited.

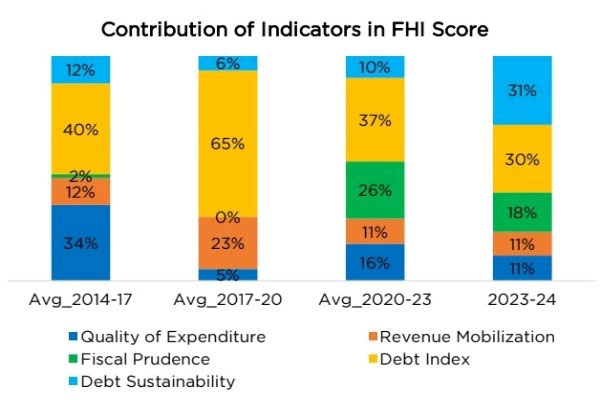

Tripura’s fiscal deficit declined sharply in 2023–24. It fell to ₹638 crore, which equals 0.8 percent of the Gross State Domestic Product (GSDP).

In comparison, the deficit stood at ₹1,513 crore or 2.14 percent of GSDP in 2022–23. As a result, the state kept the deficit comfortably below the 3 percent FRBM ceiling.

The revenue account has remained in surplus for three consecutive years. The surplus increased from ₹570 crore in 2022–23 to ₹2,196 crore in 2023–24. This rise reflects stronger fiscal discipline.

Sustainable Growth: The 5% Drop in Tripura’s Debt-to-GSDP Ratio

Total liabilities increased from ₹17,846 crore in 2019–20 to ₹22,507 crore in 2023–24.

However, the debt-to-GSDP ratio declined during the same period. It dropped from 32 percent to 27 percent, indicating better debt sustainability.

Interest payments also declined. They accounted for 6 percent of revenue receipts in 2023–24, compared with 8 to 10 percent between 2019–20 and 2022–23.

Revenue receipts reached ₹20,538 crore in 2023–24. This marks a 12 percent increase over the previous year.

Tax revenue formed the largest component, contributing 55 percent of the total receipts.

Grants-in-aid followed with 43 percent. Meanwhile, non-tax revenue accounted for only 2 percent.

Tax revenue grew by 9.57 percent during the year. At the same time, non-tax revenue increased by 4.73 percent, while grants-in-aid rose by 7.94 percent.

Within the tax category, taxes on income and expenditure contributed the highest share at 46 percent.

Goods and Services Tax (GST) followed with a 36 percent share.

However, the state’s own tax collection remained relatively modest. It formed only 29 percent of total tax revenue, while the remaining 71 percent came from the Union tax share.

Of the total receipts:

- Tax revenue accounted for 55%

- Grants-in-aid made up 43%

- Non-tax revenue contributed only 2%

Total tax revenue grew by 9.57%, while non-tax revenue rose 4.73% and grants-in-aid increased 7.94%.

Shift in Spending: 90% of Capital Expenditure Now Targeted at Social & Economic Sectors

Revenue expenditure increased by 37 percent between 2019–20 and 2023–24.

This growth gave the government greater room for development spending.

During 2023–24, expenditure on general services rose by 8 percent. Spending on economic services increased slightly by 1.6 percent.

However, expenditure on social services recorded a marginal decline of 1.5 percent.

Capital expenditure, on the other hand, increased sharply. It grew by 35 percent compared to the previous year.

Nearly 90 percent of this investment went to social and economic sectors, which shows a clear focus on development-oriented projects.

Expenditure During 2023–24:

- General services expenditure grew by 8%

- Economic services increased by 1.6%

- Social services recorded a marginal decline of 1.5%

- Capital expenditure recorded a sharp 35% increase over the previous year.

- Nearly 90% of this spending went to social and economic sectors.

Committed expenditure, which includes salaries, pensions and interest payments, also increased.

It rose by 19 percent between 2019–20 and 2023–24. However, its share in total revenue expenditure declined from 68 percent to 59 percent. This decline indicates gradual fiscal consolidation.

Transparency Hurdles: Addressing the ₹960 Crore Utilization Certificate Gap.

As of March 31, 2024, about ₹550.14 crore remained parked in Drawing and Disbursing Officer (DDO) bank accounts.

In addition, 2,867 utilisation certificates worth ₹960.87 crore were still pending.

These issues reduce transparency in expenditure management. They may also affect the credibility and timeliness of financial reporting.

Fiscal outcomes vary widely across Indian states. States such as Odisha continue to lead due to controlled deficits and stable revenues.

In contrast, Punjab, Kerala, West Bengal and Andhra Pradesh face persistent fiscal pressure because of rising debt and continued deficits.

Among the North Eastern and Himalayan states, Arunachal Pradesh leads with strong expenditure quality and prudent debt management. Uttarakhand also performs well due to higher mobilisation of its own revenue.

For the common man in Tripura, this ‘Achiever’ status is more than just a boardroom statistic. Even so, the 35% surge in capital expenditure directly correlates with the accelerated infrastructure projects seen across construction of school and hospitals across the State. This will benefit the common people of the State However, the 2% non-tax revenue figure suggests that the state may soon need to explore new avenues for internal revenue generation to maintain this momentum.